Senior Citizens and Taxes: Maximize Your Benefits

How to Navigate Senior Taxes

Save Money and Maximize Your Retirement Income

Retirement marks the beginning of a joyful and carefree chapter in life. However, navigating the world of taxes can be complex, especially with the tax changes during our senior years. Understanding what taxes you must pay and the potential benefits and exemptions available is crucial for effective financial management in retirement.

This guide aims to simplify the intricacies of federal and state taxes for our senior years, providing essential information to help you optimize your income and minimize your tax burden during retirement.

Federal Taxes for Senior Citizens

When it comes to federal taxes, senior citizens face specific obligations and potential exemptions that differ from the general population. Grasping these specific tax rules can enable you to better manage your finances and potentially lower your tax obligations.

Will My Social Security Benefits Be Taxed?

As of 2024, up to 40% of seniors may have a portion of their Social Security benefits taxed. Whether your benefits are taxed depends on your combined income—a measure the IRS uses to assess tax liability. This calculation is crucial for seniors to understand, as it directly impacts whether or not you'll owe taxes on your benefits.

How to Determine if Your Social Security Benefits are Taxable

Your combined income is calculated as follows:

Adjusted Gross Income (AGI): This represents your total earnings from various sources, including employment income, retirement benefits, investment income, and other revenue, after applying allowable deductions.

Non-taxable Interest Income: This includes interest earned from state and local bonds, which is not subject to federal tax.

Half of Your Social Security Benefits: Add 50% of your total Social Security benefits to your AGI and non-taxable interest income.

Formula:

Combined Income = AGI + Non-taxable Interest Income + (50% of Social Security Benefits)

Once you have your combined income, compare it to the IRS thresholds to determine if your benefits are taxable.

Let’s take a look at the details:

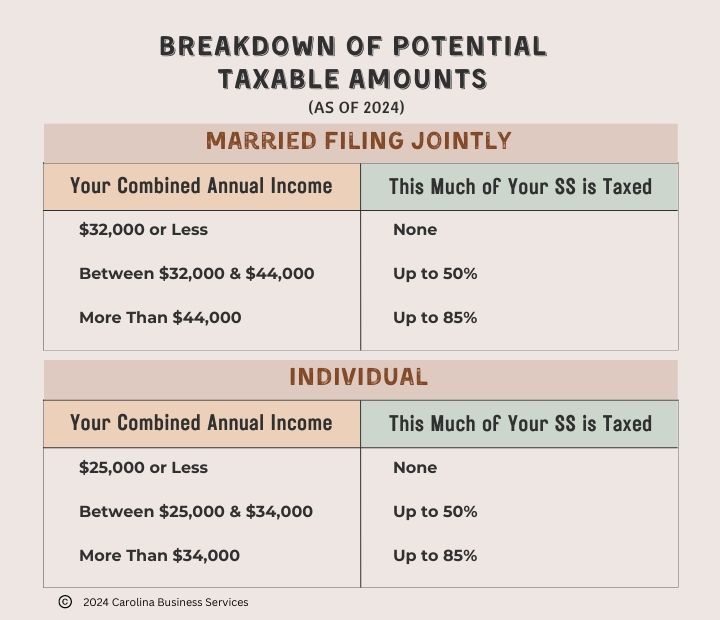

Breakdown of Potential Taxable Amounts

The IRS uses your combined income to determine the taxable portion of your Social Security benefits:

As of 2024

Single filers:

- If your combined income falls between $25,000 and $34,000, up to half of your benefits may be taxed.

- If it's over $34,000, up to 85% could be taxable.

Married couples filing jointly:

- The combined income range for potential taxation is between $32,000 and $44,000 for up to 50% of your benefit.

- If it exceeds $44,000, up to 85% could be taxed.

Married filing separately: You'll likely owe taxes on your benefits regardless of income.

Additional Resources:

Want to avoid a tax surprise? Consider having federal income taxes withheld directly from your Social Security benefits. This helps ensure you avoid owing a large sum come tax time.

Need more information?

- Social Security Administration's comprehensive guide.

- IRS publication on social security benefits.

- Must I pay income tax on Social Security Benefits. Ask Rusty - Association of Mature American Citizens (AMAC)

Important Notes:

- IRS Annual Threshold Changes: The thresholds for determining the taxability of Social Security benefits can change yearly, so it's essential to stay updated on the current limits.

- Not All Benefits Are Taxable: Depending on your combined income, it’s possible that none, part, or all of your Social Security benefits will be taxed.

- State Taxes Vary: While this section focuses on federal taxes, be aware that state taxes on Social Security benefits can differ significantly. Some states, such as Florida and Texas, do not tax Social Security benefits at all.

Navigating Retirement Income:

Taxes and Strategies

Retirement Account Withdrawals

When you withdraw money from your retirement accounts like IRAs and 401(k)s, you generally have to pay taxes on the amount you take out. This is because these accounts offer tax advantages while your money is growing, but the withdrawals are considered taxable income.

It's important to plan your withdrawals carefully. Once you reach a certain age, typically 73, you must start taking money out of your retirement accounts, even if you don't need it. This is called a Required Minimum Distribution (RMD). Failing to withdraw the required amount can result in significant penalties.

Early withdrawals, taken before age 59 ½, often come with a 10% penalty in addition to regular income tax. There are some exceptions to this penalty, but it's generally best to avoid early withdrawals if possible.

By planning your withdrawals wisely, you can help minimize your tax burden and ensure your retirement savings last as long as you need them.

Pension Income: Tax Implications

Receiving pension income can provide financial stability in retirement, but it's important to understand the tax implications.

Federal Income Tax on Pensions:

- Traditional pensions: If you contributed to your pension with pre-tax dollars, the entire amount you receive is generally taxable.

- Other pension plans: Tax treatment varies depending on how the plan was funded.

- IRS: Topic no. 410, Pensions and annuities

State Taxes: State tax laws on pension income differ. Check your state's tax rules to see if your pension is taxable.

Managing Your Pension Income: To avoid surprises at tax time:

- Tax withholding: Ensure enough taxes are withheld from your pension.

- Estimated taxes: If needed, make quarterly estimated tax payments.

- Seek advice: Consult a tax professional for personalized guidance.

Understanding how your pension is taxed can help you make informed financial decisions in retirement.

Managing Investment Income

Investment income, such as stock dividends, interest from bonds, and capital gains from selling investments, can affect your taxes. Some investments, like municipal bonds, are tax-free. Others, like stocks and bonds, are often taxable.

Capital Gains: Profits from selling investments are called capital gains. Holding investments for over a year usually results in lower taxes compared to short-term gains.

Tax-Saving Strategies:

- Diversify your investments: Balancing taxable and tax-free investments can help manage your overall tax bill.

- Time your sales: Selling investments strategically can reduce your tax burden. For instance, selling losing investments to offset gains can be beneficial.

- Consider tax-advantaged accounts: Utilize retirement accounts like IRAs and 401(k)s to potentially lower your taxes on investment growth.

- Seek professional advice: A financial advisor is invaluable for creating a personalized investment plan that minimizes your tax liability.

Understanding these factors and implementing effective strategies can protect your investment returns and maximize your after-tax income.

State Taxes for Senior Citizens

Navigating state taxes can be complex, as laws vary widely. Many states offer tax breaks for seniors, including property tax exemptions, income tax deductions, and sales tax relief on certain items. However, the specific benefits available depend on where you live. Please visit your particular state's tax agency website to discover the tax breaks you may qualify for, in addition to consulting a tax professional.

Now, let's explore federal tax obligations and benefits for seniors.

Tax Credits and Deductions for Seniors

Your tax bill can be significantly reduced by utilizing tax credits and deductions. Here are some critical benefits for seniors:

Senior Citizen Tax Credit: You may qualify for the Senior Citizen Tax Credit if you're 65 or older and meet specific income requirements. This credit directly reduces your tax bill, potentially providing substantial savings.

Medical and Dental Expense Deduction: Seniors often have higher healthcare costs, including prescriptions, doctor visits, and dental care. Typically, you can deduct the excess cost of these expenses over 7.5% of your adjusted gross income.

Higher Standard Deduction: Seniors qualify for a higher standard deduction compared to younger taxpayers. While this can simplify your tax return, comparing it to potential itemized deductions is essential to determine the most beneficial option.

Maximizing Your Tax Benefits

- Itemize carefully: If your medical expenses or other deductions exceed the standard deduction, itemizing could result in significant savings.

- Claim all eligible deductions: If applicable, ensure you claim deductions for property taxes, state income taxes, and charitable contributions.

- Seek professional advice: A tax professional can assist you in identifing all available credits and deductions and optimize your tax situation.

You can maximize your retirement income using these tax breaks and working with a professional tax advisor.

Expert Tax Assistance for Seniors

Navigating the complexities of senior taxes can be overwhelming. Carolina Business Services offers expert tax preparation tailored to seniors' unique needs. Our team provides fast, efficient, and personalized service, ensuring you feel cared for and your tax benefits are maximized. Visit our website, www.CarolinaTaxServices.com, for valuable tax resources and learn how we can help you navigate your senior taxes with ease.

Final Thoughts on Navigating Senior Taxes

Understanding your tax obligations as a senior is crucial for maximizing your retirement income. By taking advantage of available credits and deductions, staying informed about tax changes, and consulting with a professional tax preparer or CPA when needed, you will confidently navigate the complexities of taxes.

Remember: Tax laws can change, so it's essential to review your situation regularly. Consider consulting with a tax professional to ensure you're making the most of your tax benefits.

Disclaimer: The information provided in this article is intended for general income tax knowledge and informational purposes only. It does not constitute professional financial or tax advice. Individual financial circumstances vary, and consulting with a qualified tax professional is recommended to address specific tax-related questions and make informed decisions.

Stay Tuned: Big Changes Ahead for Seniors in 2025 🛑

Exciting news is on the horizon for senior citizens! The incoming 2025 U.S. President has announced plans to make significant changes to Social Security benefits, including a proposal to eliminate taxes on these benefits. This could mean:

- More Money in Your Pocket: If Social Security benefits are no longer taxed, seniors could see a significant boost in their disposable income.

- Simplified Tax Filing: Removing taxes on benefits may streamline the tax process for many retirees.

💡 What You Can Do Now:

- Stay informed by following updates on tax legislation.

- Consult with a tax professional to prepare for potential changes in your 2025 tax planning.

Remember to Bookmark this guide for the latest insights and updates!

2024 Frequently Asked Questions about Seniors and Taxes

Do Seniors Have to File Taxes?

Whether you need to file taxes as a senior depends on your income level and filing status. Generally, if your gross income exceeds the standard deduction plus additional amounts for seniors, you must file. For example, a single filer over 65 with income over $14,700 must file a federal return (2023-2024).

Are There Any Age-Related Tax Benefits for Seniors?

Yes, seniors can benefit from a higher standard deduction, the Senior Citizen Tax Credit, and various state-specific exemptions and deductions. These benefits aim to reduce the tax burden on older adults.

How Can Seniors Reduce Their Taxable Income?

Seniors can reduce their taxable income by taking advantage of available deductions, such as medical expenses, and credits like the Senior Citizen Tax Credit. Properly managing retirement account withdrawals and investing in tax-exempt assets can also help.

What if my income changes during the year?

If your income fluctuates, your tax liability may also change. It's important to monitor your combined income and consult a tax professional if you’re unsure about your tax obligations.

How do I report Social Security income on my tax return?

ButtonYou’ll receive a Social Security Benefit Statement (Form SSA-1099) each January, which you’ll use to report your benefits when filing your taxes.

Taxing Times

Get In Touch

About Carolina Business Services

For over 40 years, our firm has been a trusted provider of income tax preparation services to individuals and small businesses across Spindale, Rutherfordton, and Forest City, NC. Our vast expertise and knowledge allow us to handle tax preparations - from simple to complex - across all 50 states and for US citizens living abroad.

Our personalized and efficient tax preparation services are designed with you in mind, and our friendly and fast approach means you can count on us to work for you.

So why wait?

Contact us today!

Centrally Located

Rutherford County, North Carolina

Copyright © 2023 Carolina Business Services - All Rights Reserved.